GET-THE-BEST-RATE

PAY OFF your Mortgage in ~7 YEARS!

Get Professional Advanced Mortgage Advice - FREE!

Reduce Interest cost by ~$248,000 on a $600,000, Mortgage.

Master your Mortgage for Financial Freedom!

Working with Home Buyer's and Home Owner's in BC, and across Canada.

Follow My Three Step Plan

To Get The Ultimate Mortgage!

Get started right away

The best place to start is to connect with me directly. My commitment is to listen to your needs, assess your financial situation, provide professional mortgage advice, and

guide you through the mortgage process.

Get clarity

Sorting through all the different mortgage lenders, rates, terms, and features can be overwhelming.

Let me cut through the noise. I'll outline the best mortgage products available with your needs in mind.

Proceed with confidence

My goal is to make sure you know exactly where you stand at all times. From your initial application through your mortgage renewal, I'm available to answer any questions for as long as you need a mortgage.

I've got you covered.

Dean Garrett

Your Home Mortgage Interest is

NON-TAX DEDUCTIBLE

Convert your Home Mortgage into a

TAX-DEDUCTIBLE

loan AND pay off your mortgage in record time.

All without straining your current finances.

You don’t have to increase your required payment to ACHIEVE INCREDIBLE RESULTS!

Get started by completing my online mortgage application.

I'll let you know exactly where you stand so you can proceed with confidence.

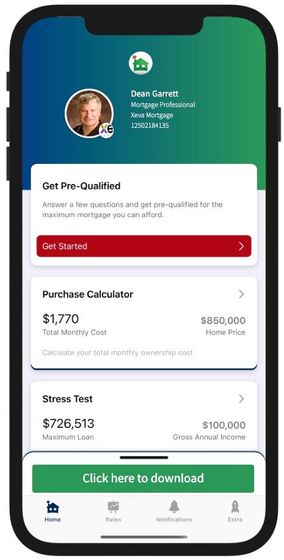

Download my Mortgage Toolbox App

What you can do with my app

Calculate your total cost of owning a home

Estimate the minimum down payment you need

Calculate Land transfer taxes and the available rebates

Calculate the maximum loan you can borrow

Stress test your mortgage

Estimate your Closing costs

Compare your options side by side

Search for the best mortgage rates

Email Summary reports (PDF)

Use my app in English, French, Spanish, Hindi, and Chinese

Everything you need,

all in one place

As a trusted mortgage provider, let me help you with these services.

Click through any of the services to learn more

Purchase

Refinance

Renewal

First Time Home Buyers

Self Employed

Next Home

Investment

Older Canadians

Divorce Mortgage

Mortgage articles to keep you informed.

Go ahead and schedule a meeting with me!

Contact Information

Dean Garrett

Mortgage Professional

104-1995 Cliffe Ave.

Courtenay BC

V9N2L2

BCFSA #146309

Send a Message

Send A Message

Thank you for contacting me.

I will get back to you as soon as possible.

Oops, there was an error sending your message.

Please try again later.

All Rights Reserved | VERICO - XEVA Mortgage LLP